What You Need to Know: what credit score needed for mortgage for Maryland buyers

- Justin McCurdy

- Dec 29, 2025

- 15 min read

So, what’s the magic number? What credit score do you actually need to get a mortgage? While there's no single answer that fits everyone, the general benchmark for most conventional loans is a score of 620 or higher.

But don't panic if your score isn't quite there yet. You still have options! Programs like FHA loans can open the door to homeownership for buyers with scores as low as 580. In fact, our lender partner can go as low as a 580 credit score, and they'll even help you build your credit for free if you're not quite there.

What Your Credit Score Really Means for a Mortgage

Think of your credit score as your financial report card. It’s a friendly three-digit number, usually somewhere between 300 and 850, that gives lenders a quick snapshot of how you’ve handled debt in the past. A higher score basically tells them you’re a reliable borrower, which makes them much more comfortable lending you a large sum of money.

This number is a huge deal when you're buying a home. It directly impacts whether you get approved for a mortgage and, just as importantly, how much that loan will end up costing you. It’s one of the very first things a lender will check.

Where Do You Stand?

It helps to know where your score falls in the grand scheme of things. Lenders group scores into different tiers, from excellent to poor, and knowing your range gives you a realistic idea of what to expect.

A great score doesn't just get you approved; it can literally save you tens of thousands of dollars over the life of your loan through a lower interest rate. For example, a buyer with a 740 score might get an interest rate that's a full percentage point lower than a buyer with a 640 score. On a $350,000 loan, that difference could save them over $200 every month! It's one of the most powerful tools in your home-buying toolkit.

Our lender partners get it—everyone's financial story is unique. They offer loan programs for buyers with credit scores starting as low as 580 and even provide free credit-building help to get you ready for a mortgage.

A lot of people get discouraged because they think they need a perfect credit score to buy a house. That's just one of the many myths of buying a new home in Maryland we help our clients bust through. The truth is, there’s a lot more flexibility than you might think.

Whether you’re looking in White Marsh, Edgewood, Baltimore County, or Harford County, understanding your credit is the first step toward your dream home—a home where you get to pick out your own flooring, countertops, and cabinets.

How a Strong Credit Score Saves You Thousands

Imagine you're in our design studio, using my proprietary visualization tools to map out your dream kitchen. You’re choosing the perfect quartz countertops, the exact shaker-style cabinets, and picturing your family gathered around a new island. Now, think of your credit score as the financial key that makes this entire vision more affordable.

Getting approved for a mortgage is just the starting line. A strong credit score does something far more powerful—it can save you a staggering amount of money over the life of your loan. We're not talking about abstract percentages here; this is real cash that stays in your pocket.

The Real-World Impact of Your Score

When lenders see a high credit score, they see a reliable borrower. To compete for your business, they'll offer you a lower interest rate, which is simply the fee you pay to borrow their money. It might not seem like a big deal, but even a small difference in that rate adds up to huge savings.

Let’s look at a practical example. Say two different buyers in Maryland are looking to finance a $400,000 home. One has an excellent credit score of 760, while the other's is a fair 630. The buyer with the 760 score might get an interest rate of 6.5%, while the buyer with the 630 score gets a rate of 7.5%. The first buyer's monthly payment would be about $2,528, but the second buyer's would be $2,797. That's a difference of $269 every single month!

For many people, a few points on a credit score can feel insignificant, but in the world of mortgages, those points translate directly into thousands of dollars. Improving your score is one of the best investments you can make in your homebuying journey.

This becomes especially important when you’re planning all the custom touches for your new home. The money you save on interest could go directly toward upgraded flooring, that luxurious primary bathroom you’ve been eyeing, or the smart home features that make everyday home living easier. It gives you more breathing room to create the home you’ve always wanted.

A Tale of Two Mortgages

Let's crunch the numbers and see how this plays out. We'll compare two homebuyers, both applying for a $400,000 loan for their dream home in a community like White Marsh or Edgewood.

Buyer A has a 760 credit score. This is considered excellent. Lenders are eager to work with them and will offer their best possible interest rates.

Buyer B has a 630 credit score. They can still get approved, but lenders see this as a higher risk and will assign a higher interest rate to match.

For a long time, a 620 FICO score has been the magic number for a conventional mortgage. But recent data shows just how much that score matters. Borrowers with top-tier scores of 760-850 land an average APR of 7.242% on a 30-year fixed loan. Meanwhile, those in the 620-639 range face a much steeper 7.838%.

What does that look like for a $400,000 loan? The homebuyer with the 760+ score pays around $2,832 per month. But the buyer with the 620-639 score is looking at a $2,911 payment. That difference adds up to over $28,000 in extra interest in just the first five years. You can discover more mortgage insights based on credit scores to see the full picture.

That $28,000 is money that could have finished a basement, decked out your kitchen with high-end appliances, or built a beautiful backyard patio. It’s a powerful reminder that your credit score isn’t just a number; it’s a tool that unlocks significant savings and more possibilities for your new home.

The best part? Your score isn't set in stone. Our lender partners can often work with scores as low as 580 and will even help you build your credit for free. They offer personalized guidance to put you in the best possible financial position, so you can save money and move into the customized home you deserve in Baltimore County or Harford County.

Choosing the Right Loan for Your Credit Score

Diving into the world of mortgages can feel like you're trying to crack a secret code, with all the acronyms flying around—FHA, VA, USDA, what does it all mean? Don't worry, I've got your back. Think of me as your personal translator for all things home loans.

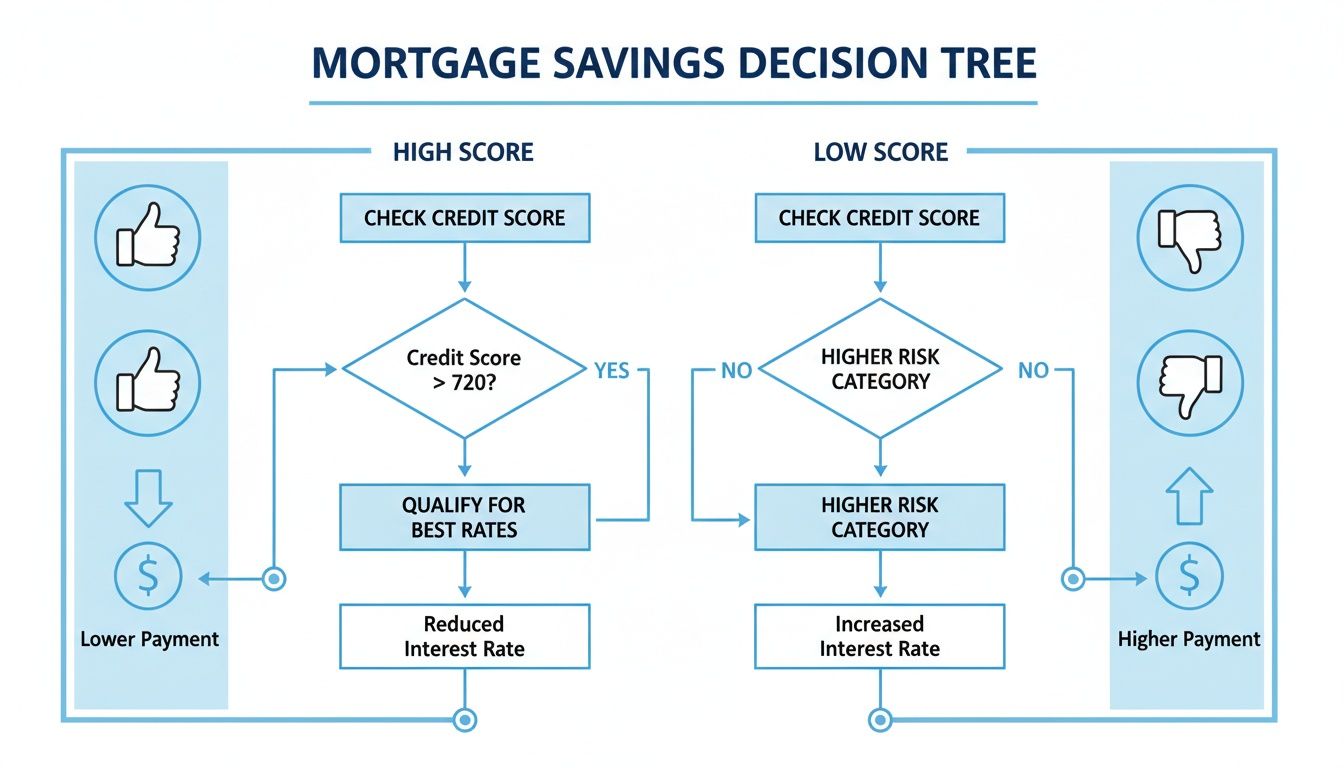

Let’s break down the most common loan types and figure out which one makes the most sense for you. Whether you're a first-time buyer eyeing a new home in Harford County or ready to put down roots in Baltimore County, there’s a path to homeownership waiting for you. The key is matching your credit score to the right financing.

This decision tree gives you a great visual of how a higher credit score directly translates to lower payments, while a lower score can mean shelling out more each month.

As you can see, putting in a little work to boost your credit score is one of the smartest money moves you can make. It can save you thousands over the life of your loan.

FHA Loans: Your Flexible Path to Homeownership

FHA (Federal Housing Administration) loans are a real game-changer, especially if you're just starting out or your credit isn't quite perfect. Because they're government-insured, lenders are much more comfortable working with borrowers who have lower scores.

This opens up a world of possibilities. For example, our lender partners can often help buyers get approved for an FHA loan with a credit score as low as 580. This single program has helped so many people in our communities, from White Marsh to Edgewood, finally get the keys to a brand-new, customized home.

An FHA loan is designed to make homeownership more accessible. With lower down payment requirements and flexible credit guidelines, it's often the key that unlocks the door for buyers who thought they weren't ready.

Now, there is one thing to know about FHA loans: they require a Mortgage Insurance Premium (MIP). This is basically an insurance policy that protects the lender if a borrower can't make their payments. But for many new homeowners, it’s a totally worthwhile trade-off to start building equity sooner rather than later.

Conventional Loans for Stronger Credit Profiles

Conventional loans are what most people think of when they hear the word "mortgage." They aren't backed by the government, which means they come with stricter requirements. Lenders typically look for a credit score of 620 or higher and often expect a larger down payment than FHA loans.

If you’ve built a solid credit history, a conventional loan is probably your best bet. You’ll almost always get a better interest rate. Plus, if you can put down at least 20%, you get to skip mortgage insurance altogether, which lowers your monthly payment right from the start.

It's a fact of the market: a strong FICO score is your best tool for getting favorable loan terms. While some standards have loosened up recently, a score of 620 is still the general benchmark for conventional loans, with FHA stepping in for scores down to 580 (with a 3.5% down payment). It’s good to know, though, that only about 15-20% of borrowers actually qualify at that lower FHA threshold because of the higher risk. You can always see the latest Federal Reserve data on lending standards to stay informed.

Specialized Loans: VA and USDA

For some buyers, there are even more powerful loan programs available that are tailored to specific situations.

VA Loans: If you're an active-duty service member, a veteran, or an eligible surviving spouse, this is an incredible benefit. Guaranteed by the U.S. Department of Veterans Affairs, these loans almost always require zero down payment and have no private mortgage insurance.

USDA Loans: Backed by the U.S. Department of Agriculture, these loans are designed to help people buy homes in designated rural and suburban areas. Just like VA loans, they often come with no down payment requirement, making them a fantastic option for buyers in qualifying communities.

Finding the right loan is a huge step, but you don't have to figure it all out on your own. I'm proud to connect my buyers with some of the best in the business. Check out how our Maryland lender partners can help you secure financing for your new home—they are absolute pros at matching you with the perfect loan for your financial picture.

How New Credit Scoring Models Can Help You Qualify

The whole world of credit scoring is getting a much-needed upgrade, and honestly, it’s fantastic news if you’re thinking about buying a new home. For a long time, the system felt a bit stuck in the past, but now, newer, smarter models are finally coming into play.

This isn't just a minor update. We're talking about a real shift in how lenders see your financial picture. Models like FICO 10T and VantageScore 4.0 are built to look at more of your actual financial life, giving a fairer and more accurate read on how you handle your money.

A Fairer Way to Look at Your Finances

So, what’s the big deal with these new models? The main difference is they can finally consider financial data that older systems just ignored. This is a huge win for people who've always been responsible with their money but might not have a long history with things like credit cards or car loans.

For example, these new scores can actually look at your history of paying rent on time. If you've been a reliable renter for years in places like Edgewood or White Marsh, that good behavior can finally help prove you're a solid borrower. It’s a common-sense change that lets lenders see the real you.

This shift in credit scoring is all about opening the door to homeownership for more people who might have been stuck on the edge of approval. It's an exciting change that makes the dream of owning a home you can customize more reachable than ever.

What This Means for Maryland Homebuyers

If you're looking at homes here in Maryland, this is a pretty big deal. A major change is on the horizon for 2025, when the Federal Housing Finance Agency (FHFA) will start using these new models. Both FICO 10T and VantageScore 4.0 will also use a "bi-merge" approach, meaning they'll pull data from two credit bureaus instead of all three, which should lead to more consistent and fair scores.

This update could genuinely change the game for mortgage approvals. VantageScore 4.0, in particular, is expected to score 10-20% more people by including non-traditional data like rent payments—a massive leg up for first-time buyers. You can dig into the details of how these new credit score initiatives are changing the landscape for homebuyers.

What this all boils down to is that your consistent, responsible habits—even the ones outside of traditional loans—can now help you get a mortgage. It’s a move toward a more balanced system that acknowledges all the smart financial things you do.

Even with these positive changes, I get that credit can be a headache. That’s why our lender partners not only work with scores as low as 580 but also offer to help you build your credit score for free. They’ll look at your specific situation and map out a plan to get you in the best possible shape to buy the home you’ve been dreaming of.

Let's get you ready to start picking out your new countertops and flooring.

Ready to Boost Your Credit Score? Here’s How.

If your credit score feels like a roadblock on your path to a new home, don't worry. This isn't just theory—we’re diving into practical, real-world steps you can take right now to get that number climbing.

First, you need to know what you’re working with. Lenders look at five main things: your payment history, how much debt you carry, the age of your credit accounts, recent credit inquiries, and the types of credit you have. Let’s tackle them one by one.

Nail Your Payment History

This is the big one. Your payment history makes up a whopping 35% of your FICO score. Lenders need to see that you reliably pay your bills on time, every time. Even one late payment can cause a serious dent in your score.

Set It and Forget It: Autopay is your best friend. Set it up for at least the minimum payment on all your loans and credit cards to guarantee you're never late.

Give Yourself a Nudge: If you’re not a fan of autopay, use calendar alerts or a budgeting app to send you reminders a few days before each due date.

A late payment can haunt your credit report for up to seven years, so making on-time payments a habit is absolutely critical.

Tame Your Credit Utilization

Next up is your credit utilization ratio, which accounts for about 30% of your score. This is just a fancy term for how much of your available credit you're actually using. For a practical example, if you have a $10,000 credit limit and a $5,000 balance, your utilization is 50%.

A great rule of thumb is to keep your credit utilization below 30% on each card and overall. Lenders see high utilization as a sign of financial stress, so paying down balances is one of the fastest ways to boost your score.

A huge piece of this puzzle is getting your debt under control. For some excellent strategies, check out these 7 steps to pay off debt fast. It’s a fantastic guide for building a smart, effective plan.

To make things even clearer, I've put together a simple checklist to guide you.

Your Credit Score Improvement Checklist

Here's a straightforward checklist of actions you can take to start improving your credit score today. Focusing on these items will have the biggest impact on how lenders see your creditworthiness.

Action Item | Why It Matters | Pro Tip |

|---|---|---|

Review Your Credit Reports | You need to find and dispute any errors. An incorrect late payment could be dragging you down. | Get your free reports from all three bureaus (Equifax, Experian, TransUnion) annually. |

Pay Every Bill on Time | Payment history is 35% of your score. Consistency is key to building trust with lenders. | Use autopay or calendar alerts. No exceptions! |

Pay Down Credit Card Balances | Lowering your credit utilization (the amount you owe vs. your limit) gives your score a quick boost. | Aim to get all cards below a 30% utilization ratio. Paying it down just before the statement date helps. |

Avoid Closing Old Accounts | Older accounts increase the average age of your credit history, which is a positive factor. | Keep that old, no-fee card open even if you only use it for a small recurring charge to keep it active. |

Limit New Credit Applications | Each application for new credit can result in a hard inquiry, which can temporarily dip your score. | Only apply for credit you truly need, especially in the months leading up to a mortgage application. |

Tackling these steps one by one will put you in a much stronger position when it's time to talk to a lender.

You Don't Have to Do This Alone

Figuring all this out can feel like a lot, but you’re not on your own. I believe everyone deserves a clear path to the home of their dreams, which is why I've teamed up with some truly exceptional lender partners.

They do more than just process loans; they provide a genuine support system. If your score isn't quite mortgage-ready, they will work with you to build your credit—for free. They’ll sit down, go over your report with you, and map out a personalized game plan. It’s a hands-on service designed to put you in the driver's seat.

Getting your credit in shape brings you one step closer to the fun part—using my proprietary visualization tools to pick out the perfect floors, cabinets, and countertops for your new home in White Marsh, Edgewood, or anywhere in Baltimore and Harford Counties. For more tips on navigating this process, be sure to read our guide on the do's and don'ts of buying a new home in Maryland.

Ready to Start Your Maryland Home Journey?

You've done the homework on mortgage readiness, and now for the fun part—actually getting started. The path to a new home can feel like a maze, but let's boil it down to one key idea: your credit score is a big deal, but it's never a permanent roadblock.

Think of a lower score as a starting point, not a final destination. In fact, our trusted lending partners are often able to work with scores as low as a 580, opening doors you might have assumed were locked shut.

Your Path to a Truly Customized Home

While the builder I represent provides high-quality homes, I go a step further—offering my clients unique proprietary visualization tools, hands-on service, and access to visualizers that help you bring your dream space to life. We give you this access in fantastic communities like White Marsh, Edgewood, Baltimore County, and Harford County.

Picture yourself designing your kitchen—choosing the perfect flooring, cabinets, and countertops—with a dedicated team cheering you on every step of the way. If you want a full overview of the entire process, this guide on the steps to buying your first home is a great place to start.

Your dream home isn't some far-off fantasy. It's right here, within reach, and I'm ready to help you find it. Whether your credit is sparkling or needs a little TLC, our partners will craft a personalized plan for you—completely free.

Let’s Build Your Future, Together

What's next? A simple, friendly conversation. No pressure, no strings attached. Whether you're eager to jump into my visualizer tools and start designing your ideal bathroom or just want to chat about what’s possible, I'm here for it.

Don't let questions about what credit score is needed for a mortgage keep you on the sidelines. Let's connect and start turning your vision into a blueprint for your new life.

Frequently Asked Questions About Mortgage Credit Scores

Buying a home is a huge step, and it's totally normal to have a million questions—especially when it comes to credit scores. Let's tackle some of the most common questions I hear from aspiring homeowners right here in Maryland.

Can I Get a Mortgage with a 580 Credit Score?

Yes, you absolutely can! It might sound on the lower side, but getting a mortgage with a 580 credit score is more than possible. Our lender partners work with FHA loan programs that are specifically designed to help buyers in this exact situation.

While a higher score will always land you better interest rates, a 580 can be the key that opens the door to your new home. It puts homeownership within reach for a lot of people who thought they were still years away from qualifying.

How Long Does It Take to Improve My Credit Score for a Mortgage?

This really depends on your unique financial situation, but many people start seeing real progress in just 3 to 6 months. The quickest wins usually come from two things: paying all your bills on time, every time, and lowering your credit card balances.

Even small, consistent steps can add up fast. The best part? Our lender partners offer free credit-building services to create a personalized game plan just for you, helping you get mortgage-ready even quicker.

Do Lenders Use the Same Credit Score I See on Credit Karma?

That's a fantastic question, and the short answer is no, not quite. The free credit monitoring apps you use, like Credit Karma, are great for keeping a general eye on things. They typically show you a VantageScore.

Mortgage lenders, however, almost always use a specific version of your FICO score that's built for home lending. So, the number the lender sees might be a little different from the one on your app. The only way to know for sure is to connect with a lender for a pre-qualification.

Don't be surprised if the score your lender pulls is a few points different from what your app shows. This is completely normal and part of why working with a knowledgeable lender is so important. They can explain the differences and what your specific score means for your loan options.

Will Shopping for a Mortgage Hurt My Credit Score?

This is a common fear, but you can breathe easy on this one. The credit scoring models are built to understand that you're shopping for a single, major loan—not trying to open a dozen new credit cards.

As long as you do all your mortgage rate shopping within a focused timeframe, usually 14 to 45 days, all those inquiries from different lenders will count as just one single event on your credit report. This minimizes the impact, so feel free to compare your options to find the best deal.

For more answers to your homebuying questions, check out our full list of FAQs for Maryland new homebuyers.

Ready to take the next step toward a home you can truly make your own? I provide a unique, hands-on experience, complete with proprietary visualization tools that bring your dream space to life. Let’s have a conversation about how you can start picking out your countertops, flooring, and cabinets in a beautiful new home in White Marsh, Edgewood, or throughout Baltimore and Harford Counties. Start your journey today.

Comments