How to get pre approved mortgage in Maryland: A quick guide

- Justin McCurdy

- Nov 4, 2025

- 13 min read

If you're thinking about buying a home, getting pre-approved for a mortgage isn't just a good idea—it's the single most important first step you can take. Think of it as the official green light from a lender, a letter confirming they’re ready to loan you a specific amount of money. This simple piece of paper transforms you from a casual browser into a serious, qualified buyer, giving you a massive advantage before you even start looking at houses.

Why Pre-Approval Is Your Home Buying Superpower

Before you fall in love with a home in White Marsh or start daydreaming about a new life in a Baltimore County community, getting that mortgage pre-approval is your secret weapon. It stops you from just guessing and turns your search into a focused, confident mission. It's truly your golden ticket to homeownership.

Gain a Serious Competitive Edge

Picture this common scenario in Harford County: a fantastic home comes on the market, and two couples immediately put in an offer. One couple attaches their pre-approval letter, while the other says they’ll get their financing sorted out later. Which offer do you think the seller is going to take seriously? Almost always, it’s the pre-approved buyer.

That letter is your proof that you’re financially ready to close the deal. In today’s market, where you might be up against multiple offers, that pre-approval can be the one thing that makes your offer shine and get accepted.

Understand Your True Budget

It’s so easy to get swept up in beautiful online listings, but without knowing what you can actually afford, you're just setting yourself up for heartbreak. A pre-approval gives you a real, concrete price range to work with. For instance, you might think you can afford a $450,000 home, but a pre-approval could reveal your comfortable budget is actually closer to $425,000. That's not bad news—it's powerful information that lets you focus your search.

A mortgage pre-approval isn’t just about qualifying for a loan; it’s about giving you the clarity and confidence to shop for a home that fits comfortably within your financial life.

This clarity allows you to zero in on homes that are truly within your reach, saving you a ton of time and emotional energy. When you know your numbers from the very beginning, you make smarter, more confident decisions.

Pre-Qualification vs. Pre-Approval

It's really important to know the difference here, because they are not the same thing. A pre-qualification is a quick, informal guess a lender gives you based on financial info you tell them yourself. It's not verified.

A pre-approval, on the other hand, is the real deal. It’s a much deeper dive where the lender actually verifies your:

Income and employment history

Credit score and full credit report

Assets (like savings and investments) and existing debts

Because it's a verified commitment from the lender, a pre-approval carries so much more weight with sellers. It also makes the closing process way faster, since most of the heavy financial lifting is already done. With this powerful tool in your back pocket, you’re ready for the fun part—finding your dream home in places like Edgewood or Prince George's County.

Gathering Your Financial Documents for Pre Approval

Alright, let's talk paperwork. This is the part that trips a lot of people up, but it doesn't have to be a headache. Think of it less as a chore and more like building your case—you're showing the lender you're a reliable borrower who's ready for this.

Getting your documents in order before you even talk to a lender is a huge pro move. It shows you’re serious and organized, and honestly, it just makes the whole process go a thousand times faster. I usually recommend creating a dedicated digital folder on your computer to store everything. That way, when your lender asks for something, you can send it over in minutes.

What Lenders Really Want to See

So, what exactly are they looking for? Lenders need to verify three main things: your income, your assets (what you own), and your debts (what you owe). It’s all about creating a complete financial snapshot.

Here’s a quick rundown of the essentials you’ll need to pull together:

Proof of Income: Grab your pay stubs from the last 30 days. You’ll also need your W-2s from the past two years to show a consistent work history.

Tax Returns: Lenders will want to see your federal tax returns for the last two years. If you're self-employed, this is especially important—be ready with your profit and loss statements, too.

Bank and Asset Statements: You'll need the last two to three months of statements for all your accounts. This means checking, savings, 401(k)s, IRAs, you name it. They need to see where your down payment is coming from. If you're still building up your funds, our guide on how to save for a down payment has some great tips.

Personal ID: This one’s easy—just a clear copy of your driver's license and your Social Security number.

To make it even simpler, here's a checklist you can use to track everything you need.

Your Essential Mortgage Pre Approval Document Checklist

Having these documents ready will make the application process much smoother. Lenders appreciate a borrower who comes prepared.

Document Category | What You Need | Why It's Important |

|---|---|---|

Identification | Driver's License or State ID, Social Security Number | Verifies your identity and allows for a credit check. |

Income Verification | W-2s (past 2 years), Pay stubs (past 30 days), Federal Tax Returns (past 2 years) | Confirms your employment is stable and your income can support the loan. |

Asset Verification | Bank Statements (2-3 months), Investment/Retirement Account Statements (401(k), IRA) | Shows you have the funds for the down payment and closing costs. |

Debt Information | Credit Report, Info on other loans (auto, student), Alimony/Child Support Orders | Gives the lender a full picture of your existing financial obligations. |

Once you have this folder of documents ready, you'll feel much more confident heading into the next steps.

Why Every Document Tells a Story

Each piece of paper serves a specific purpose. Your W-2s and pay stubs are the proof of your steady paycheck. Your tax returns offer a wider-angle lens on your finances, which is critical if your income isn't a simple salary.

Your bank statements are probably the most scrutinized documents. Lenders use them to confirm you have the cash for the down payment and closing costs. They'll also be on the lookout for any large, out-of-the-ordinary deposits. For example, if your grandma gave you a generous $5,000 gift for your down payment, you'll need a signed "gift letter" from her explaining that the money is a gift, not a loan that needs to be repaid. Knowing how to get your bank statement online is a simple but crucial first step here.

My biggest tip? Get this all organized before you apply. It does more than just speed things up—it puts you in control of the conversation with lenders.

When you're prepared, you project confidence. It tells lenders you're a low-risk, responsible borrower, and that can only help your case. Once you get that pre-approval letter, the real fun starts. You can start seriously looking at homes in White Marsh or Edgewood, knowing exactly what your budget is. And that's when I can step in with my hands-on service and proprietary visualization tools, helping you see how you could pick your own flooring, countertops, and cabinets to make a house truly your own.

What Lenders Are Really Looking For

Ever wonder what a loan officer is really thinking when they pull up your application? It’s not some big secret. They’re just trying to answer one fundamental question: "Can I count on this person to pay back this loan?"

To get to that answer, they focus on a few key areas of your financial life.

It all boils down to three big things: your credit, your capacity, and your capital. Think of them like the legs of a stool—if one is shaky, the whole thing gets a bit wobbly. Lenders want to see strength across the board before they hand over a huge chunk of cash.

Your Credit History And Score

This is almost always the first thing a lender checks. Your credit score is a quick, easy way for them to see how you've handled debt in the past. You don't need a perfect score, but a higher one definitely helps you snag a better interest rate.

And hey, don't sweat it if your score isn't quite where you want it. There are plenty of ways to bump it up before you even apply. For some solid, actionable tips, check out our guide on the credit score for a home loan and how to boost your chances. Just focusing on paying bills on time and keeping your credit card balances low is a fantastic start.

Your Capacity To Repay The Loan

Next up is capacity, which is just a fancy way of asking, "Can you actually afford this monthly payment?" Lenders figure this out by calculating your debt-to-income (DTI) ratio, and trust me, this number is a big deal.

Your DTI is simply the percentage of your gross monthly income that goes toward paying your monthly debts.

Let's make it real with a practical example:

Say you and your partner bring in a combined $7,000 a month before taxes.

Your other monthly debts (like a car payment, student loans, and credit card minimums) add up to $1,500.

In this scenario, your DTI is $1,500 / $7,000 = 21.4%.

Most lenders want to see a DTI of 43% or lower for a conventional loan after factoring in your potential new mortgage payment. This gives them confidence that you won't be stretched too thin and will have enough cash left over for, you know, life. Our lender partners can go up to a DTI of 57% for FHA Loans.

Your Capital And Assets

Finally, lenders need to see you've got some capital. This is your cash on hand for the down payment and closing costs. This is exactly why they ask for all those bank statements—they want to see proof that you have a financial cushion.

Having a healthy savings account shows lenders you're financially responsible and ready for the realities of homeownership, which go way beyond just the mortgage payment.

If you can think like a lender, you can spot potential red flags in your own application before they do. The good news is that lenders approved about 85.89% of mortgage applications in recent years. Getting pre-approved is your best move to make sure you’re in that group. It acts as a dry run that dramatically lowers your chances of a surprise rejection later. You can dig into more of these fair lending statistics on homebuyer.com if you're curious.

And once you have that pre-approval in hand, I can bring my hands-on service and proprietary visualization tools to the table to help you design the perfect home in one of my communities in White Marsh or Harford County.

Navigating the Mortgage Pre-Approval Process

Alright, so you're ready to make your move. Let's walk through what the pre-approval journey actually looks like, from the first application to getting that letter in hand. Think of this less like a formal set of instructions and more like a friendly guide to get you through it with confidence.

To make this real, let’s imagine a couple, Maria and David, who are finally ready to buy their first place in Edgewood, Maryland. They’ve done the hard work of saving up and getting their paperwork in order, and now it’s time to find a lender.

Finding Your Perfect Lender

The first big decision for Maria and David is where to even apply. There are a few different routes they can take, and each one has its own feel:

Big Banks: You know the names. These national players have a massive menu of loan products and slick online applications. The trade-off? The experience can sometimes feel a bit impersonal, more like a number than a name.

Local Credit Unions: Since they're member-owned, credit unions often bring a more personal touch. You might find better rates and more flexible terms, especially if you're already a member.

Mortgage Brokers: Think of a broker as your personal mortgage shopper. They have relationships with dozens of lenders and do the legwork to find the best fit for you. This can be a huge time-saver and a stress-reducer.

Maria and David decide to play it smart. They applied with our lender partner, Clint Kohler with First National Bank (which is almost like a local bank) and our mortgage broker partner, Mark Miller with Guild Mortgage. This lets them compare offers and feel confident they’re getting the best deal.

Submitting Your Application

Whether you fill out a form online in your PJs or sit down with a loan officer in person, the application itself is pretty straightforward. You'll hand over all the documents we've talked about and give the lender the green light to check your credit.

Now, about that credit check. It's important to understand what is a hard credit pull and its impact on your finances. Yes, this inquiry will cause a temporary dip in your score by a few points. But don't sweat it. The credit bureaus are smart enough to know you're shopping for a mortgage. They treat multiple inquiries within a 14-45 day window as a single event.

Once you hit "submit," expect a loan officer to reach out with a few follow-up questions. They might ask Maria and David to explain a recent large deposit in their savings account or why an old address is still showing up on their file. The key is to be honest and get back to them quickly.

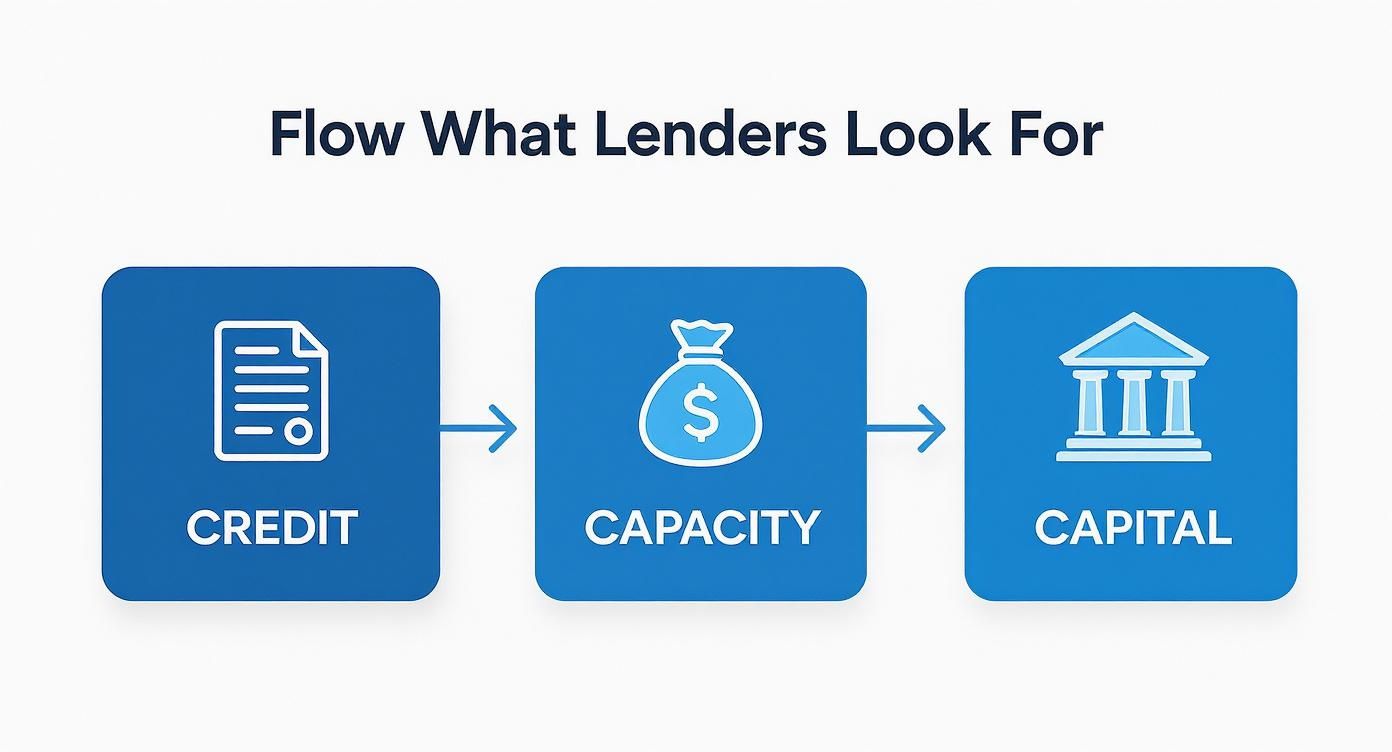

This infographic breaks down the three core things any lender is going to zero in on.

It really is that simple. Lenders want to see your track record with debt (Credit), your ability to actually make the monthly payments (Capacity), and the cash you have on hand for the down payment and closing costs (Capital).

A successful pre-approval isn't about having a flawless financial record. It's about presenting a clear, honest, and reliable picture that gives the lender confidence in you as a borrower.

The whole process, from application to pre-approval letter, can take anywhere from a few days to about a week. The more organized you are with your documents, the faster things will move.

It’s also worth noting that even with today's home prices, pre-approval activity is actually buzzing. In a recent quarter, some digital mortgage platforms reported an 11.9% increase in pre-approval letters issued over the previous quarter, with younger, first-time buyers driving much of that growth. You can discover more insights on these mortgage trends to get a feel for the current market.

While pre-approval is a huge step, it's often confused with pre-qualification. They aren't the same thing, and we break it all down in our friendly guide to getting prequalified for a mortgage loan.

You’re Pre-Approved! So, What Happens Next?

Congratulations! Holding that pre-approval letter in your hand is a huge moment. This document is your green light to start your house hunt with real confidence, but the race isn't quite finished. Now, the name of the game is protecting that pre-approval while you search for the perfect place.

Think of your pre-approval letter as more than just a number. It clearly lays out your approved loan amount, the likely interest rate, and any other conditions the lender has set. Knowing these details helps you zero in on homes that are comfortably within your budget, which is key to avoiding heartbreak and last-minute stress.

Keep Your Pre-Approval Status Locked In

I tell all my clients to treat the time between getting pre-approved and closing on their home as a "financial quiet period." Your lender gave you the thumbs-up based on a specific snapshot of your finances. Any big moves now can raise a red flag and put your final loan approval in jeopardy.

Here’s a simple list of "don'ts" to live by while you're shopping for a home:

Don’t make any big-ticket purchases. Now is not the time to finance a new car or rack up credit card debt on furniture. Any new debt will alter your debt-to-income ratio, which is a major red flag for lenders.

Don’t open or close credit cards. Opening new credit can cause a temporary dip in your credit score. Believe it or not, closing old accounts can also hurt your credit by impacting your history's length and utilization ratio.

Don’t switch jobs or how you get paid. Lenders love stability. Even if a new job comes with a raise, it can create uncertainty for underwriters who need to see a consistent and reliable employment history.

Don’t deposit large, untraceable sums of cash. Every dollar needs a paper trail. A big deposit that you can't explain might look like you took out another loan from a friend or family member, which lenders need to know about.

The best advice I can give is simple: keep your financial life as boring and predictable as possible until the keys to your new home are officially in your hand.

Now for the Fun Part

With your pre-approval secured, this is where the excitement really begins. You can start exploring amazing Maryland communities in places like Prince George's County or Harford County with the confidence of a serious buyer.

The market is buzzing. In a recent year, total mortgage originations hit about $2.3 trillion, a surge driven by well-prepared buyers just like you. Being ready makes all the difference in a competitive market.

This pre-approval is your foundation. But I take it a step further with hands-on service and my unique visualization tools. We can use your approved budget to bring your dream space to life, letting you virtually pick out everything from countertops to flooring and tile. Together, we can find a house and truly make it your home.

For a full rundown of what comes next, be sure to check out our complete step-by-step home buying Maryland guide.

Got Questions About Mortgage Pre-Approval? We've Got Answers.

Jumping into the mortgage pre-approval process always brings up a few questions. It's a huge financial step, so that's completely normal! Let's walk through some of the most common things homebuyers ask, so you can move forward with confidence.

How Long Is a Pre-Approval Good For?

Think of your pre-approval letter as having an expiration date. Most are valid for about 60 to 90 days. Why? Because your financial picture can change. Lenders need to know that your income, credit, and assets are still solid when you're ready to make an offer.

If your house hunt takes a bit longer, don't sweat it. Renewing your pre-approval is usually pretty straightforward. You'll just need to give your lender some updated paperwork—like your latest pay stubs and bank statements—to show that you're still in the same great financial shape. A quick check-in with your loan officer is all it takes.

Will Getting Pre-Approved Wreck My Credit Score?

This is probably the number one worry I hear, and the short answer is: not really. When you apply, the lender does a "hard inquiry" on your credit report, which might cause a small, temporary dip of a few points.

But here's the good news. The credit bureaus know that smart buyers shop around for the best mortgage rates.

That's why they treat multiple mortgage inquiries within a short period (usually 14 to 45 days) as just a single event. The power you gain as a pre-approved buyer is well worth the tiny, short-lived hit to your score.

Should I Get Pre-Approved by More Than One Lender?

One hundred percent, yes! This is a pro move that can save you a serious amount of money over the long haul. You wouldn't buy the first car you test drive, right? The same logic applies here.

Getting pre-approved with two or three different lenders lets you lay all their offers out on the table and see who's really giving you the best deal. You can compare:

The interest rates they're quoting.

Their specific closing costs and fees.

The different loan programs they offer.

Just make sure you get all those applications in within that 14-to-45-day window to minimize the credit score impact. Doing this little bit of homework puts you in the driver's seat, ensuring you get the best financing for your new home, whether you're looking in White Marsh or anywhere in Baltimore County.

Once you have that pre-approval letter in hand, the fun part begins. At Customize Your Home, I do more than just help you find a great house. I offer a hands-on service with unique visualization tools that let you see your dream home before you even move in. We let you pick the perfect flooring, countertops, cabinets, and tile, making sure the home you buy is a true reflection of you. Let's start bringing your vision to life today. Find out how at https://www.customizeyourhome.com.

Comments