Home Loan Types Explained for Maryland Buyers

- Justin McCurdy

- Nov 8, 2025

- 17 min read

Figuring out mortgages can feel like a real headache, but it’s really just about finding the loan that matches your life and finances. Think of it as a friendly chat over coffee, where we explore the main players: Conventional, FHA, VA, and USDA loans. Each one is built for different kinds of buyers, from those with perfect credit to those just starting out.

Your Guide to Maryland Home Loan Options

So, you're thinking about buying a home in Maryland—that’s fantastic! It's a huge step, but tackling the financing part can feel like you're trying to decipher a secret code. My goal here is to strip away the jargon and give you the straightforward scoop on your options.

Think of this as your friendly roadmap to choosing the right loan, whether you're looking at a new home in White Marsh, Edgewood, or anywhere else in Baltimore County and Harford County. Before we dive into the Maryland specifics, it’s always a good idea to get a handle on the general types of mortgage loans available to see the full landscape.

Finding Your Path to Homeownership

The world of mortgages is always changing. Lately, we've seen a huge wave of first-time homebuyers, especially from younger generations. In the first quarter of 2025, Gen Z buyers made up one in four first-time homebuyer loans. Many of them are using FHA loans to get their foot in the door, which is a smart move in this market.

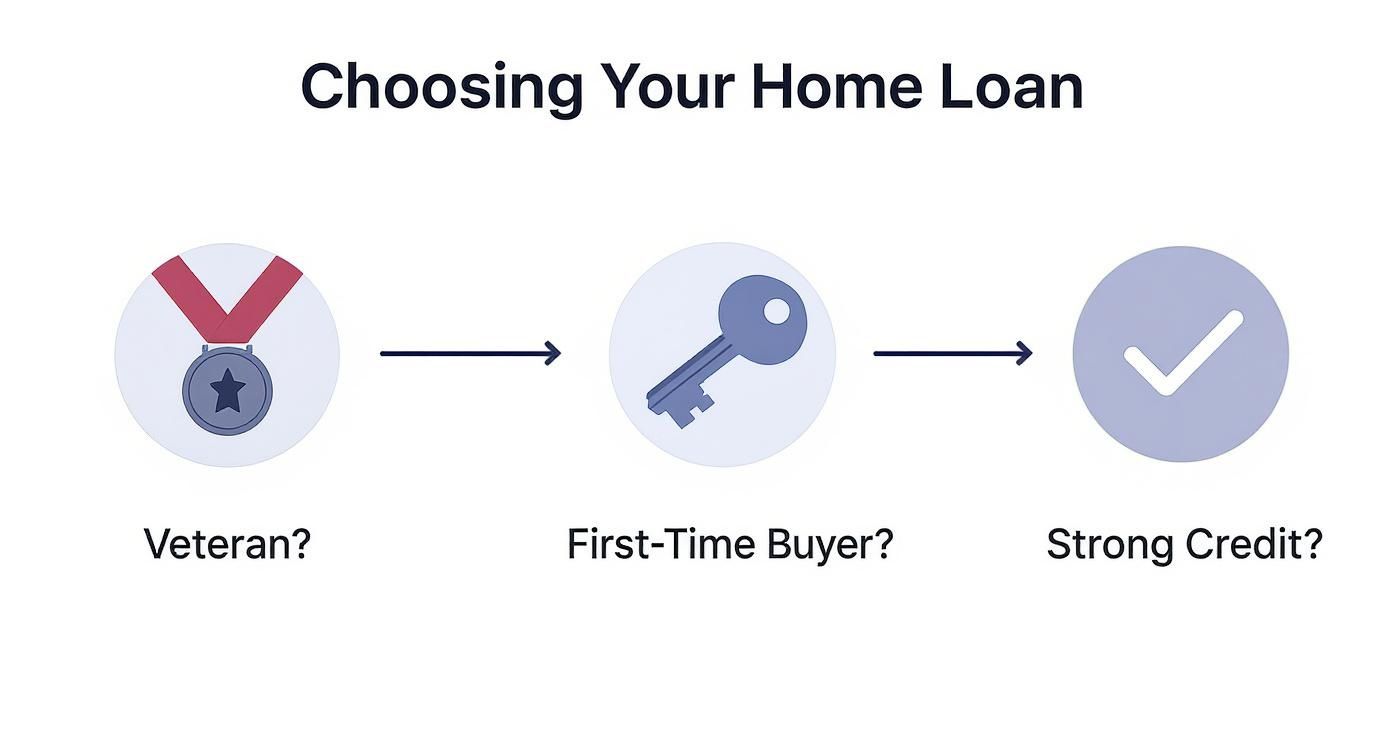

This decision tree gives you a quick visual to get you started.

As you can see, things like your credit score or whether you’ve served in the military play a big part in pointing you toward the right loan. For a more detailed walkthrough, don’t miss our complete guide on https://www.customizeyourhome.com/post/how-to-buy-your-first-home-in-maryland.

Quick Look Home Loan Comparison

To make things even easier, I've put together a simple table that breaks down the key differences. It's a great way to see how the major loan types stack up against each other at a glance.

Loan Type | Best For | Minimum Down Payment | Credit Score |

|---|---|---|---|

Conventional | Buyers with strong credit and stable finances | As low as 3% & in some of my communities 0% | Typically 620+ |

FHA | First-time buyers or those with lower credit scores | 3.5% | 580+ (sometimes lower) |

VA | Active military, veterans, and eligible spouses | 0% | No official minimum |

USDA | Buyers in designated rural/suburban areas | 0% | Usually 640+ |

This table is just a starting point, but it helps frame the conversation. Each loan has its own quirks and benefits that we'll explore in more detail.

While the builder I represent provides high-quality homes, I go a step further—offering my clients unique proprietary visualization tools, hands-on service, and access to visualizers that help you bring your dream space to life. You can mix and match flooring, countertops, and cabinets, and see it all on screen before you commit to anything. It’s a game-changer!

Conventional Loans: The Go-To Mortgage Option

When most people think of a "standard" or "regular" mortgage, they're usually talking about a conventional loan. This is the most common home loan out there, and for good reason.

Unlike government-backed loans (which we'll get to later), these aren't insured by an agency like the FHA or VA. They are the bread and butter of the private lending world—the kind of loan you'd get from your local bank, credit union, or mortgage company. Because they don't have government strings attached, they offer a ton of flexibility, making them a fantastic choice for borrowers with strong, stable finances.

The Two Main Flavors of Conventional Loans

Conventional loans aren't a one-size-fits-all product. They generally break down into two main types, and it all boils down to how much you need to borrow.

Conforming Loans: These are the most common. They "conform" to the loan limits set by Fannie Mae and Freddie Mac—the two huge government-sponsored enterprises that buy mortgages from lenders. These limits change each year to keep up with home prices, so a conforming loan in Harford County will cover the vast majority of homes on the market.

Jumbo Loans: Thinking bigger? If the house you've got your eye on requires a loan that exceeds those conforming limits, you'll be looking at a jumbo loan. Since lenders are taking on more risk with these larger amounts, they'll be a bit stricter. Expect to need a higher credit score and a more substantial down payment to qualify.

A Practical Example: Let's say a family in White Marsh with good jobs and diligent savings finds a new home for $450,000. Their strong financial history makes a conforming conventional loan their best bet. They’ll likely get a competitive rate and a straightforward process without the extra paperwork of a government program.

What to Expect for Down Payments and Credit Scores

This is where having your financial ducks in a row really pays off. While some special conventional loan programs let you put down as little as 3%, putting down more is always better.

A strong credit score is also non-negotiable. The bare minimum for a conventional loan is typically a 620 score, but the real magic happens when you get into the 700s. A higher score tells lenders you're a reliable borrower, and they'll reward you with a lower interest rate, which can save you a ton of money over the years.

Your credit score is easily one of the most powerful numbers in your financial life. It’s a snapshot of your creditworthiness, and it has a direct line to the interest rate a lender will offer you.

Taking time to polish your credit before you even start house hunting is one of the smartest moves you can make. If you want a deeper dive, you can learn more about how to boost your mortgage chances by improving your credit score.

Let's Talk About Private Mortgage Insurance (PMI)

If your down payment is less than 20% on a conventional loan, get ready to hear about Private Mortgage Insurance, or PMI in most cases. However, in some of my communities you could qualify for 0% down with no PMI and lower than market rate that is fixed for 30 years.

Don't let the name fool you—PMI is an insurance policy that protects your lender, not you. If something happens and you can't make your payments, PMI helps the lender recoup their losses. It's usually rolled right into your monthly mortgage payment, so you'll see it as a line item on your statement.

But here's the best part about PMI: it’s not permanent. This is a huge perk of conventional loans! Once you've paid down your mortgage to 80% of the home's original value, you can ask your lender to remove it. Getting rid of PMI can drop your monthly payment significantly, freeing up that cash for everything from home improvements to a vacation fund.

FHA Loans: A Flexible Path to Your First Home

Does the thought of saving up a massive 20% down payment feel completely out of reach? What if your credit score is pretty good, but not quite perfect? If you’re nodding along, you’re not alone. This is exactly where an FHA loan can be a total game-changer, opening a door to homeownership that might have otherwise seemed shut.

These loans are insured by the Federal Housing Administration, but the government isn't the one lending you the money. Instead, the FHA provides insurance to private lenders, which gives them the confidence to say "yes" to buyers who might not check all the boxes for a conventional loan. This flexibility is what makes FHA loans so popular, especially for first-time homebuyers in vibrant communities across Prince George's County and Harford County.

Who Is an FHA Loan Good For?

FHA loans were created to make buying a home more accessible. They're often the perfect fit for people who have a steady income but have struggled to save up a huge down payment or build an elite credit score.

I like to think of it this way: a conventional loan is like trying out for the varsity team—you need top-tier stats to make the cut. An FHA loan is more like the junior varsity squad; it welcomes talented players who are still developing their skills and gives them a real chance to get in the game.

Here’s who usually benefits the most:

First-Time Homebuyers: With a down payment as low as 3.5%, FHA loans seriously lower the amount of cash you need upfront.

Buyers with Lower Credit Scores: Lenders can often approve FHA loans for borrowers with credit scores starting around 580, and sometimes even a bit lower depending on the rest of your financial picture.

People with Limited Savings: That low down payment means you can get into a home much sooner without having to completely drain your savings.

The Trade-Off: Mortgage Insurance Premium

Of course, there's always a trade-off. With FHA loans, it's called the Mortgage Insurance Premium (MIP). It's similar to the PMI you'd find on a conventional loan, but with a couple of key differences. FHA loans actually require two types of MIP.

First, you've got an upfront premium that's paid at closing, which most people just roll right into their total loan amount. Then, there's an annual premium that gets broken down and added to your monthly mortgage payments. For most people taking out an FHA loan today, this monthly MIP lasts for the entire life of the loan—it doesn't just disappear once you hit 20% equity like PMI does.

This is the crucial detail to understand. While FHA loans offer an incredible on-ramp to homeownership, the long-term cost of MIP is something you need to factor into your budget.

FHA Loans in Action: A Practical Example

Let's imagine a young couple, Sarah and Tom, who are ready to buy their first home in Edgewood, Maryland. They both have stable jobs but have only managed to save $15,000. Their credit scores are sitting around 640—solid, but not quite high enough to get the best terms on a conventional loan.

They find a great starter home for $350,000. With an FHA loan, their minimum down payment is just 3.5%, which works out to $12,250. This fits perfectly within their savings and even leaves them a small cushion for moving costs and furniture. Without the FHA option, they'd have needed to save for years to get to a 20% down payment of $70,000. Thanks to the FHA loan, Sarah and Tom can move out of their apartment and start building equity in a home of their own.

Plus, government-backed loans like FHA often come with very competitive interest rates, which really helps with affordability. For instance, in October 2025, when 30-year fixed conventional rates were topping 7%, the average FHA 30-year loan was around 6.096%. You can check out more about recent mortgage rate trends to see how these numbers stack up.

VA Loans: A Powerful Benefit for Service Members

If you've served our country, the VA loan isn't just another mortgage option—it's a hard-earned benefit. Honestly, it's one of the best home financing programs out there, created by the U.S. Department of Veterans Affairs to make buying a home a reality for active-duty military, veterans, and eligible surviving spouses.

Think of it as the nation's way of saying "thank you," but with incredible mortgage terms. The headline feature, the one everyone talks about, is the ability to buy a home with 0% down. That alone removes the single biggest roadblock for most people—scraping together a huge chunk of cash for a down payment. This can make all the difference when you're looking for a home in communities like White Marsh or Edgewood.

Do You Qualify for a VA Loan?

Figuring out if you're eligible is the first step, and it's usually simpler than you might think. It all boils down to meeting specific service requirements, like serving a certain number of days on active duty or in the National Guard or Reserves.

To show a lender you qualify, you'll need a Certificate of Eligibility (COE). This is just the VA's official thumbs-up, confirming you've met the service requirements for the loan benefit. Don't sweat it; getting your COE is easy. Most lenders can pull it up for you online in a matter of minutes.

The VA Funding Fee Explained

So, VA loans don't have a down payment or monthly mortgage insurance, which is amazing. But most borrowers will pay a one-time VA funding fee. This fee is what keeps the program going for future generations of service members.

How much is it? The amount changes based on a few things:

Your type of military service (e.g., regular military vs. Reserves/National Guard)

If this is your first time using the benefit or a subsequent use

The size of your down payment, if you decide to make one

It’s also important to know that some veterans are completely exempt from this fee. This usually includes veterans receiving VA disability compensation and surviving spouses of service members who died in the line of duty or from a service-connected disability.

More Perks of the VA Loan Program

The benefits of a VA loan go way beyond just the zero-down-payment perk. These loans are packed with features designed to save you money and give you peace of mind.

One of the biggest money-savers is that there's no monthly mortgage insurance. With Conventional or FHA loans, you'd be stuck paying an extra fee every month if your down payment is less than 20%. A VA loan gets rid of that cost completely, which can seriously lower your monthly payment.

On top of that, VA loans come with some of the most competitive interest rates on the market and have limits on the closing costs lenders can charge. Because the loan is backed by the government, lenders feel more secure, and they pass those better terms on to you.

A VA Loan Story from Harford County

Let me tell you about a client of mine. I recently worked with a veteran, Michael, and his family who were moving to Harford County. After years of service and being stationed all over, they were finally ready to plant some roots. By using his VA loan benefit, Michael bought a gorgeous new home with no money down.

This meant they could use their savings for things like furniture, moving costs, and starting a college fund for their kids. The money they save every month by not having mortgage insurance gives them extra breathing room in their budget. For Michael, the VA loan wasn't just a financial product; it was the key to a stable, permanent home for his family after his service ended.

That's the real power of the VA loan program—it turns the dream of homeownership into a well-deserved reality.

USDA Loans: The Best-Kept Secret for Maryland Suburbs

What if I told you that you could buy a brand-new home with zero money down—and you don't have to be a military veteran to qualify? It sounds like a gimmick, but it's exactly what a USDA loan offers. This fantastic program often flies under the radar, but it’s designed to help people buy homes in less-dense suburban and rural communities.

When people hear "rural," they immediately picture tractors and farmland, miles from civilization. But you'd be shocked to see how many growing, popular suburbs around Baltimore County and Harford County actually make the cut. The USDA’s definition of "rural" is a lot broader than you think, putting that zero-down-payment dream within reach for tons of Maryland families.

So, How Do These Loans Actually Work?

Backed by the U.S. Department of Agriculture, the whole point of these loans is to encourage growth in designated areas. It works a lot like an FHA or VA loan—the government (in this case, the USDA) guarantees the loan for a private lender. This takes a lot of the risk off the lender’s shoulders, which is why they can offer such incredible terms to you, the borrower.

The two main perks are the 0% down payment and lower mortgage insurance fees compared to other loans. That one-two punch makes USDA loans one of the most affordable paths to homeownership out there. It’s a true hidden gem for buyers who can check a couple of specific boxes for location and income.

The Two Big Hurdles: Location and Income

Unlike most home loans that are all about your financial history, a USDA loan has two unique requirements you have to meet first.

Property Eligibility: The home has to be in a USDA-eligible area. A surprising number of sought-after communities in Baltimore County, Harford County, and even parts of Prince George’s County are on the list. The best way to know for sure is to plug an address into the USDA's official eligibility map.

Income Eligibility: These loans are specifically for households with low-to-moderate income. Your total household income can't be more than 115% of the median income for that area. The limits are actually pretty generous and change based on the county and how many people are in your family.

Of course, your credit score is still part of the equation. Lenders generally want to see a score of 640 or higher for a USDA loan. But it’s really the focus on where you buy and what you earn that makes this program stand out.

A USDA loan is a perfect example of how the government creates targeted programs to support specific community goals. By making it easier to buy in less-populated areas, it helps these communities thrive and grow.

A Practical Example: Buying in White Marsh

Let's picture a family looking to put down roots in White Marsh. They have a solid, stable income, but saving up a big down payment while paying rent has been a real struggle. They fall in love with a new home that, as it turns out, is in a USDA-approved zone.

Boom. Just like that, they don't need a down payment. All the money they’d saved can now go toward closing costs or, even better, the fun stuff—personalizing their new home. When they work with me, they can dive into my visualization tools to pick out the perfect flooring, cabinets, and countertops, and see their dream kitchen come to life right on the screen.

Suddenly, the combination of an affordable loan and powerful design tools flips the home-buying experience from stressful to genuinely exciting.

If you’re looking at homes in places like White Marsh, Edgewood, or other similar suburbs, don't dismiss USDA loans. It might just be the key that opens the door to a beautiful, customized home you thought was still years away. Let’s talk and see if this amazing program could be right for you.

Fixed-Rate vs. Adjustable-Rate Mortgages

Alright, so you've picked a loan program like Conventional or FHA. You’re one step closer, but now you have another big choice to make. Will your interest rate stay the same for the life of the loan, or will it change over time?

This is the fundamental question that separates a Fixed-Rate Mortgage (FRM) from an Adjustable-Rate Mortgage (ARM). Let's break down what that really means for your wallet.

Think of a fixed-rate loan like a long-term lease on a car. You agree to a set payment, and that’s what you pay every single month. No surprises. Your interest rate is locked in from the get-go, giving you a totally predictable payment for the next 15, 20, or 30 years.

An ARM, on the other hand, is a bit more like your electricity bill. It often starts out lower, but it can go up or down depending on market conditions. You’ll get a sweet "teaser" rate for an initial period—usually five or seven years—but after that, your rate adjusts, and your monthly payment will change right along with it.

The Stability of a Fixed-Rate Mortgage

For the vast majority of homebuyers, the fixed-rate mortgage is the go-to option, and for good reason. It's the definition of stability. The peace of mind you get from knowing your principal and interest payment will never go up is priceless.

This predictability makes budgeting a breeze. It's a fantastic choice for families in Baltimore County or Harford County who want to plant roots and build a secure financial future without sweating over what interest rates might do next. You know exactly what’s coming, month after month.

The Potential of an Adjustable-Rate Mortgage

So if fixed-rate is so great, why would anyone even consider an ARM? The main attraction is the lower initial interest rate. For the first few years, your monthly payment will be significantly less than it would be with a fixed-rate loan.

That extra cash in your pocket each month can be a huge help. An ARM can be a smart move for specific types of buyers:

You're Not Staying Long: If you’re pretty sure you’ll be moving within a few years, you can cash in on the lower payments and sell the house before the rate has a chance to adjust.

You Expect Your Income to Grow: Are you on a career track where you're confident your salary will be much higher in a few years? If so, you might feel comfortable taking on a potentially higher payment down the road.

Before making a decision, it’s always a good idea to check the current interest rates for homes to get a feel for the market.

Now, let's put these two loan types side-by-side to make the choice even clearer.

Fixed-Rate vs. Adjustable-Rate Loan Showdown

This quick comparison will help you decide which mortgage rate structure is the right fit for your financial situation and risk tolerance.

Feature | Fixed-Rate Mortgage (FRM) | Adjustable-Rate Mortgage (ARM) |

|---|---|---|

Interest Rate | Locked for the entire loan term | Fixed for an initial period, then adjusts periodically |

Monthly Payment | Stays the same (principal & interest) | Can increase or decrease after the initial period |

Best For | Long-term homeowners, budget-conscious buyers | Short-term owners, buyers expecting income growth |

Biggest Pro | Predictability and peace of mind | Lower initial interest rate and lower starting payment |

Biggest Con | Typically has a higher starting interest rate than an ARM | Risk of higher payments in the future if rates rise |

Common Loan Terms | 15-year or 30-year terms | 5/1, 7/1, or 10/1 ARMs (fixed for 5, 7, or 10 years) |

Ultimately, choosing an ARM is a calculated risk. You're betting that you'll either move or be in a stronger financial spot before that initial low-rate period ends.

Bringing Your Vision to Life

Okay, we’ve waded through all the different home loan types, and while that’s a huge first step, let's get to the fun part—actually picturing yourself in your new home. Nailing down the right financing is what gets you in the door, but a house only feels like your home when it reflects you.

This is where I do things a little differently. I don't just help you find a great house; I give my clients exclusive access to some pretty cool visualization tools that let you play designer. Think of it like a video game for your future home. You can click through different hardwood floors, see how that quartz countertop really looks with those navy blue cabinets, or swap out tile patterns in the master bath until you find the perfect one.

It completely takes the guesswork out of the design process. You get to see how all your ideas come together on-screen before anything is installed, making sure the home you end up with is the one you’ve been dreaming about.

From Digital Dream to Your Doorstep

This whole process puts you in the driver's seat. Instead of crossing your fingers and hoping it all works together, you get to customize your space with confidence, knowing it fits your personal style. It’s all about connecting the dots between the numbers and the nesting, which makes the homebuying journey way more exciting.

After all, the little details are what make a house a home—from the loan terms down to the kitchen backsplash. Speaking of those final financial details, don't forget to check out our friendly guide to closing costs on a new home.

If you’re ready to find a place you can truly make your own in White Marsh, Edgewood, or anywhere in Baltimore County, Harford County, and Prince George's County, let's talk. I'm here to guide you through both the mortgage maze and the fun of creating a home that’s 100% you.

Your Top Home Loan Questions, Answered

Jumping into the world of mortgages can feel like learning a new language. Let's clear up some of the most common questions I hear from homebuyers just like you.

Can I Get a Home Loan with Bad Credit in Maryland?

You absolutely can! It’s a common misconception that you need a perfect credit score to buy a home.

While a stellar score will get you the best interest rates, there are fantastic programs out there designed specifically for people with a few dings on their credit report. FHA loans are a perfect example—they have more forgiving requirements, opening the door to homeownership for folks all over Maryland, from Edgewood to White Marsh.

How Much Do I Really Need for a Down Payment?

The old "you need 20% down" rule is probably the biggest myth in real estate. It's just not true for most people anymore.

Putting down 20% on a conventional loan is a great way to avoid private mortgage insurance (PMI), but it's far from the only option. Some people can even get a conventional loan in some of my communities for 0% down with no PMI and a lower than market interest fixed rate. FHA loans let you get in the door with as little as 3.5% down. Even better, if you’re a veteran or are buying in a qualifying rural area, you might be eligible for a VA or USDA loan with 0% down. Yes, zero!

What's the Difference Between Pre-Qualified and Pre-Approved?

This one trips a lot of people up, but the difference is huge when you start making offers.

Think of pre-qualification as a casual first chat. It's a rough ballpark estimate of what you might be able to borrow based on a quick conversation. It’s a good starting point, but that's about it.

Pre-approval, on the other hand, is the real deal. This is where a lender digs into your finances—verifying your income, checking your credit, and looking at your assets. The result is an official letter stating they are willing to lend you a specific amount. Sellers take pre-approved buyers much more seriously.

Want the full scoop? We break it all down in our guide on how to get pre-approved for a mortgage in Maryland.

At Customize Your Home, I don't just find you a property; I help you create a home that truly feels like you. With hands-on guidance and special visualization tools, you can see everything from countertops to flooring come together before you even move in. Ready to start building your dream in Baltimore County or Harford County? Let’s talk. https://www.customizeyourhome.com

Comments