How to Finance Rental Property: Proven Strategies for Smart Investors

- Justin McCurdy

- Dec 6, 2025

- 16 min read

So, you’re ready to jump into real estate investing? It's a fantastic way to build real, long-term wealth, but almost everyone hits the same first roadblock: "How do I actually pay for an investment property?"

Figuring out how to finance a rental property really boils down to three big moves: getting your own financial house in order, knowing all your loan options, and lining up a solid down payment. This isn't just theory—it’s the practical playbook that gets deals done.

Your Roadmap to Rental Property Financing

Think of this as your personal roadmap. We're going to cut through all the confusing bank jargon and show you the real-world options investors use every day. By the end, the whole process will feel less like a mystery and more like your next smart investment.

We’ll start by breaking down the foundational methods, from the standard bank loans you've heard of to some of the more creative approaches that seasoned pros use to scale their portfolios.

Whether you're looking at a duplex in Baltimore County or a single-family home over in Harford County, getting these concepts down is what turns a dream into a set of keys in your hand.

Why Rental Properties Are Such a Smart Move

Investing in real estate is about so much more than just owning a building. It's about creating a steady stream of income and letting your equity grow while you sleep. Those monthly rent checks chip away at your mortgage, and as the property becomes more valuable, so do you. It's a powerful wealth-building machine that has worked for generations.

For example, snagging a property in a growing area like Edgewood, Maryland, doesn't just put cash in your pocket today—it sets you up for some serious appreciation down the road.

Getting a Lay of the Financial Land

Before we get into the nitty-gritty of different loans, you need to understand the big picture. Getting a loan for an investment property is a different ballgame than buying your own home. Lenders are a bit stricter, and they’re looking for a few specific things:

A strong credit score: You'll generally want a score of 680 or higher to get the best interest rates.

A healthy Debt-to-Income (DTI) ratio: Lenders need to see you can easily handle your current bills plus the new mortgage payment without breaking a sweat.

Cash in the bank: Most lenders will want to see you have enough cash reserves to cover about six months of mortgage payments after you close on the property.

Securing financing for a rental is all about showing stability. Lenders aren't just giving you a loan; they're investing in you as a business partner. They need to trust that you can manage the property and the money that comes with it.

The Power of a Personalized Rental Space

Finding the right property is only half the job. The other half is creating a space that top-tier tenants will be lining up to rent. Instead of buying a dated property that's a massive renovation project, why not find a home you can personalize from day one?

I give my clients access to unique proprietary visualization tools that let you see your investment's potential come to life. You can pick out the exact flooring, countertops, and cabinets you know will command the highest rent in communities like White Marsh. This hands-on approach makes sure your property isn't just another rental—it's a premium home that maximizes your return.

If that sounds like a better way to invest, let's connect and find a property that fits your financial goals perfectly.

Navigating Your Loan Options: From Conventional to Creative

Alright, you're getting your financial ducks in a row. Now for the big question: what kind of loan should you actually get? The world of investment property loans is a bit different from what you might be used to if you've only ever bought your own home. Lenders see these deals as business transactions, and the rules—and loan types—reflect that reality.

Let's walk through the most common ways investors in places like Baltimore County and Harford County finance their rental properties. We'll cover everything from the tried-and-true conventional routes to some of the more clever strategies out there.

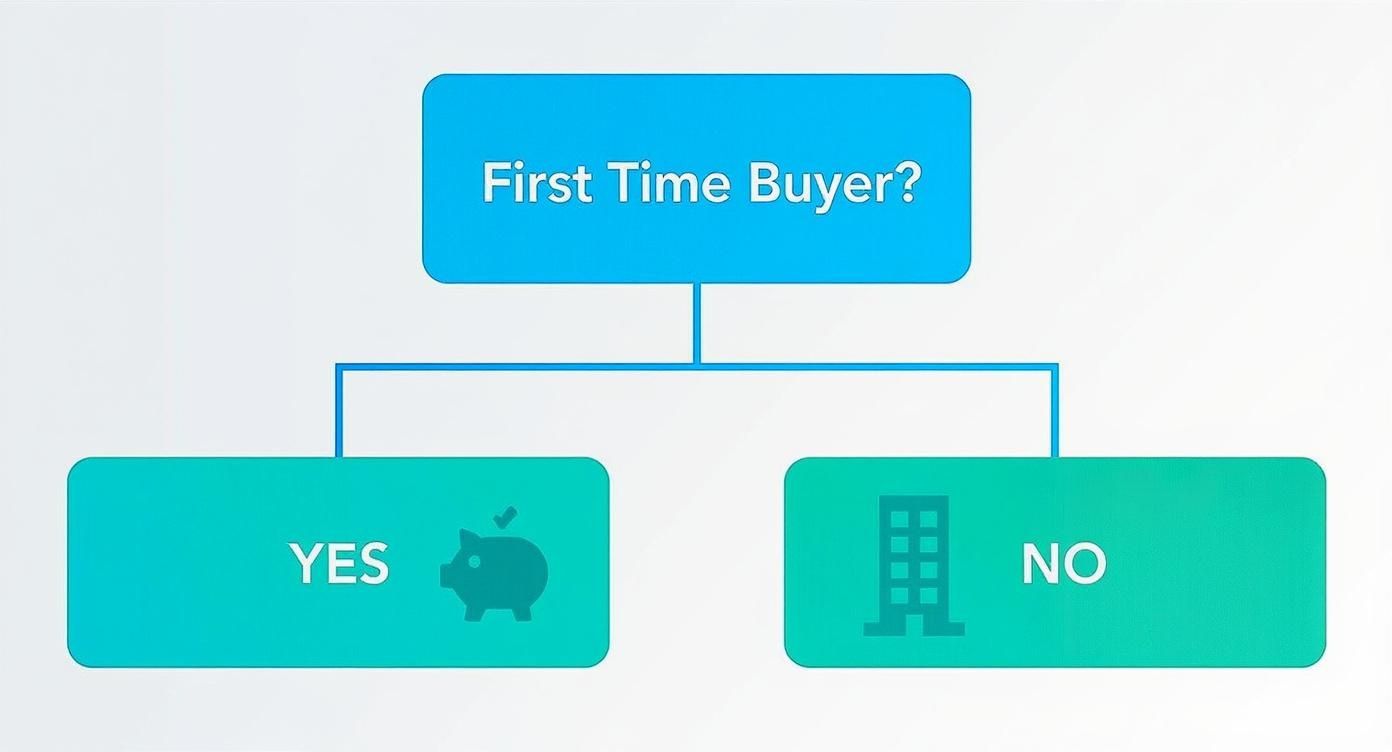

This quick visual shows how your path might look depending on whether this is your very first property or just the next one in your growing portfolio.

As you can see, new investors often stick with traditional methods, while seasoned pros might tap into their existing assets to expand their holdings. It's all about using the right tool for the job.

The Go-To Choice: Conventional Investment Loans

For most investors, the conventional loan is the industry standard. These are the workhorse mortgages offered by just about every bank, credit union, and mortgage broker. Their popularity comes from competitive interest rates and fixed terms, which keeps your monthly payment predictable and your budget on track.

But here’s where things get different for a rental property. Lenders are a bit stricter and usually require:

A higher down payment: Get ready to put down 20% to 25% of the purchase price. It’s a bigger hurdle, but it's standard for investment properties.

A solid credit score: You'll typically need a score of 680 or higher to land favorable terms. The better your score, the better your rate.

Cash reserves: Lenders want to see you have a safety net. This usually means having enough cash on hand to cover six months of mortgage payments for the new property, just in case of vacancies or surprise repairs.

Financing has always been tied to the wider economy. I remember hearing stories from older investors about mortgage rates hovering around 7-8% in the early 1980s, which made cash flow incredibly tight. We were fortunate to see rates fall below 4% in the 2010s, fueling a huge boom in rental investing as borrowing got cheaper.

Your Foot in the Door: Government-Backed Loans (FHA & VA)

Often overlooked for investing, government-backed loans can be a fantastic way to get started, especially through a strategy called "house hacking."

Here's how it works:

FHA Loans: Insured by the Federal Housing Administration, these loans let you buy a multi-unit property (up to four units!) with as little as 3.5% down, on one condition: you have to live in one of the units. You can then rent out the others, and that rental income helps cover your mortgage. It's a game-changer.

VA Loans: An incredible benefit for eligible veterans, service members, and surviving spouses. With a VA loan, you can potentially purchase a multi-unit property with zero down payment—again, as long as you occupy one of the units.

House hacking is genuinely one of the smartest ways for first-time investors to start building wealth with minimal cash out of pocket. If you want to dig deeper into these, check out our guide on home loan types explained for Maryland buyers.

Tapping Into What You Already Own: HELOCs

If you're already a homeowner, you might be sitting on a powerful financing tool without even realizing it. A Home Equity Line of Credit (HELOC) lets you borrow against the equity you've built in your primary residence. It functions a lot like a credit card—you get a revolving line of credit that you can draw from and pay back as needed.

Here's a practical example: I once worked with a buyer in White Marsh, Maryland, who wanted to grab a great rental property that just hit the market. Instead of draining their savings for a 20% down payment, they opened a HELOC on their current home. This gave them the cash for the down payment and closing costs, letting them snap up an income-producing asset without touching their emergency fund.

More Advanced Financing Tools

As your portfolio grows, you'll start looking at more specialized loan types.

Portfolio Loans: Once you have a few properties under your belt, some lenders will offer a portfolio loan. This loan bundles all your properties under a single, streamlined mortgage. It simplifies your payments and can sometimes offer better terms than juggling a bunch of separate loans.

Hard Money Loans: Think of these as short-term loans from private investors, not big banks. They are "asset-based," which means the lender cares more about the property's potential value than your personal credit score. The interest rates are higher, but the funding is fast—sometimes in just a few days. This makes them perfect for fix-and-flip investors who need to close a deal now.

Ultimately, the right loan depends on your financial situation, your long-term goals, and the specific property you're buying. Understanding all your options is the first step to choosing the path that will set you up for success.

Getting Your Financial House in Order

Before you even think about scrolling through property listings, let’s talk about the most important step: getting your own finances ready for a lender. Lenders are all about managing risk, and a borrower who has their act together is a much safer bet.

Think of it this way: you're building a financial resume. The more polished and professional it looks, the more confident a lender will be in you. This is your game plan for walking into a bank or broker's office ready to get approved.

First Up: Your Credit Score

Your credit score is the first thing any lender will pull. It’s their instant snapshot of how you handle your financial obligations. When it comes to investment properties, the standards are a bit higher than for a primary home.

Lenders generally want to see a score of 680 or higher to even consider you, but the best interest rates? Those are usually reserved for folks with scores topping 740.

A lower score isn’t a deal-breaker, but it almost always means you'll pay a higher interest rate, which cuts directly into your monthly cash flow. If your score needs some work, don't sweat it. You can absolutely improve it. For a deeper dive, check out what a good credit score for a home loan looks like and how to boost your chances.

Tame Your Debt-to-Income Ratio

Next on the list is your Debt-to-Income (DTI) ratio. It’s a simple but powerful number: your total monthly debt payments (think car loans, student loans, credit cards) divided by your gross monthly income. Lenders use this to gauge whether you can truly afford another mortgage payment without being stretched too thin.

Insider Tip: Most lenders draw the line at a total DTI—including your new rental property mortgage—of 43%. If you can get it under 36%, you'll look like a rock-star borrower.

Getting your DTI down is straightforward. You either need to increase your income or, more realistically for most people, decrease your debt. Paying down a high-interest credit card or knocking out a small personal loan before you apply can make a world of difference.

The Importance of Cash Reserves

Lenders need to see that you have a safety net, especially for an investment property. What happens if your tenant moves out and it takes a few months to find a new one? That's where cash reserves come in.

Most lenders will require you to have at least six months of the property's total mortgage payment (that’s principal, interest, taxes, and insurance, or PITI) sitting in a liquid account. And this is after you’ve paid the down payment and all your closing costs. It's proof that a leaky roof or a short vacancy won't send you into a financial tailspin.

Get Your Paperwork in a Row

There's nothing more frustrating than having your loan application stall because you're digging through old file cabinets for a two-year-old tax return. Do yourself a favor and get everything organized before you apply.

Here’s the doc-prep checklist I give all my clients:

Proof of Income: Your two most recent pay stubs, W-2s from the last two years, and your full federal tax returns (all schedules included) for the last two years.

Asset Statements: Your two most recent statements for all checking, savings, brokerage, and retirement accounts.

Debt Information: A clean list of all your current debts with lender names, account numbers, and minimum monthly payments.

Identification: A clear copy of your driver’s license and Social Security card.

Walking in with a neat folder of all this stuff shows the lender you're organized, serious, and ready to go.

It’s also worth noting another key metric lenders look at: the Debt Service Coverage Ratio (DSCR). This ratio is more about the property's ability to pay for itself, but having your personal finances in stellar shape gives lenders the confidence that you can manage the property effectively, ensuring it hits the DSCR targets they need to see.

Smart Ways to Handle Your Down Payment

Let's be real: for most aspiring investors, the down payment is the single biggest thing standing between them and their first rental property. It can feel like a mountain, but with the right game plan, it's a lot more doable than you might think. We're going to break down some practical and creative ways to get over that hurdle.

First things first, you have to set realistic expectations. This isn't like buying your own home where you might squeak by with a tiny down payment. Investment properties play by a different set of rules. Lenders see them as a higher risk, so they’ll almost always require 20% to 25% down.

Don't let that number scare you off. Knowing your target is the first step toward hitting it. The trick is to start thinking beyond just saving a little from each paycheck.

Looking Beyond Your Savings Account

While consistent saving is the bedrock of any good plan, there are other ways to build that down payment fund much, much faster. You might have access to cash you haven't even considered.

Here are a few common strategies I’ve seen successful investors use:

Gift Funds from Family: A lot of loan programs are perfectly fine with you using money gifted from a close relative. The lender will just want a formal "gift letter" confirming the money is a true gift, not a secret loan that has to be repaid. It’s a fantastic way to get a big boost.

Tapping Your Home Equity: If you already own your home, the equity you've built is a powerful tool just sitting there. A Home Equity Line of Credit (HELOC) or a cash-out refinance on your primary residence can free up the exact funds you need for a rental property down payment.

Borrowing from Your 401(k): This one requires some thought, but many employer-sponsored retirement plans let you take out a loan against your balance. It can be a quick source of cash, but you really need to weigh the pros and cons, since you'll be paying interest (to yourself) and could miss out on market gains.

The real goal is to piece together a strategy that fits your life. For so many people, it's not just one thing. It's often a combination of personal savings, a gift from parents, and a small HELOC that finally gets them across the finish line.

Making the Numbers Real

Talking in percentages is one thing, but it’s hard to wrap your head around. Let's make it concrete with a practical example from a popular Maryland community.

Imagine you've found a great potential rental in Edgewood, Maryland, for $300,000. Here’s how the cash you’d need at the closing table would likely break down:

Purchase Price: $300,000

Down Payment (20%): $60,000

Estimated Closing Costs (3%): $9,000

Total Cash Needed to Close: $69,000

Suddenly, that intimidating concept becomes a clear goal: $69,000. Now you can build a specific, actionable plan to hit that number. If you want more tips on building up your funds, you might find our guide on how to save for a down payment for your new home really helpful.

Once you’ve got a handle on the down payment, it's time to find the perfect property. In growing areas like Harford County and Baltimore County, a newer home can be a brilliant move. You get to sidestep immediate repair costs and can even customize finishes like flooring and countertops to attract top-tier tenants from day one. That's my specialty—helping investors use visualization tools to design a profitable rental before a single wall even goes up.

Thinking Beyond the Bank: Creative Financing Ideas

So, what happens when the bank’s cookie-cutter loan options just don't fit? Maybe your income is a little unconventional, or a killer deal just popped up that needs you to move faster than a traditional lender ever could. This is where the real fun begins.

When the front door is locked, you find a side window. Thinking outside the box isn't just a backup plan; it's often the strategy that unlocks the best deals and helps you build a portfolio faster than you ever thought possible.

The Power of Partnerships

Let's be real: coming up with a 20% down payment on your own is tough. This is exactly why teaming up is one of the most popular and effective ways to get into the game. Why go it alone when you can combine forces?

A partnership can solve a ton of problems at once. Maybe you’ve got the cash saved up, but your buddy has the squeaky-clean credit and W-2 income that lenders love. Boom. Together, you’re the ideal borrower. You pool your strengths, cover each other's weaknesses, and suddenly that duplex that was out of reach is well within your grasp.

Practical Scenario: Picture two friends, Sarah and Tom, eyeing a $400,000 duplex in Baltimore County. On their own, neither can swing the $80,000 down payment. But by pooling their savings, they've got it covered. They set up a simple LLC, draft a clear partnership agreement about who does what and how profits are split, and they're off to the races. They just cut their individual risk in half and got into a deal they couldn't have done alone.

When the Seller Becomes the Bank

Here's another great one: seller financing. It's exactly what it sounds like—the person selling you the house becomes your bank. Instead of writing a check to Wells Fargo every month, you’re sending it directly to the previous owner.

It's a classic win-win. The seller gets a nice, steady monthly income stream (often at a better interest rate than a CD) and can often sell their property faster without the hassles of a traditionally financed buyer. For you, the buyer, it means flexibility. You can negotiate everything directly: the down payment, the interest rate, even the length of the loan.

Don't just shake hands on it, though. You absolutely need a real estate attorney to draft a formal promissory note and a deed of trust. This protects everyone and keeps the whole arrangement professional and legally sound.

The BRRRR Method: Building a Portfolio from Scratch

If you hang around real estate investors long enough, you're going to hear about the BRRRR method. It’s not just a financing tactic; it's a full-blown strategy for building a rental portfolio with very little of your own money left in the deals.

Here’s how it breaks down:

Buy: You find a property that needs some love—a fixer-upper—and buy it below market value, often with a short-term loan like hard money.

Rehab: You roll up your sleeves (or hire someone who will) and renovate the place, forcing its value way up.

Rent: Once it's looking sharp, you find great tenants and get that cash flow rolling in.

Refinance: Now you head to a traditional bank. They'll appraise the property at its new, much higher value, and you do a cash-out refinance.

Repeat: You use that tax-free cash from the refi to pay back your initial loan, get your original down payment back, and—here's the magic—use the leftover funds for the down payment on the next property.

The "Refinance" step is the secret sauce. By creating value with the renovation, you can often pull out every single dollar you put in, and sometimes even more. You’re basically recycling the same pot of money to buy property after property.

This strategy is especially powerful right now. The global housing market is facing a massive supply crunch, with a net shortage of 6.5 million housing units in major developed economies alone. This is pushing millions of people into the rental market, creating incredible demand. You can see for yourself how this global living shift is fueling the rental boom.

This intense demand means a freshly renovated rental in a community like White Marsh or Edgewood is a golden goose. Tenants are lining up for quality places to live. I actually help investors get a leg up by offering unique visualization tools that let you play with different finishes—flooring, cabinets, countertops—to design a premium rental that commands top dollar from day one.

Finding and Perfecting Your Investment Property

Alright, you’ve got your financing squared away. Now for the exciting part—the hunt for the perfect property. This is where a great partner can make all the difference, helping you turn a good deal into a fantastic, long-term investment.

Instead of endlessly scrolling through listings for a place that almost works, imagine creating a property that’s perfectly designed to attract top-tier tenants from the moment it’s ready. This approach is a game-changer, especially in high-demand Maryland areas like White Marsh and Edgewood where quality rentals are always snapped up quickly.

Customize to Maximize Your Rental Income

Seasoned investors know a secret: the right finishes don't just look good, they command higher rent. A home with sleek, durable flooring, bright quartz countertops, and modern cabinets isn't just another rental listing—it's a premium product that stands out.

When you find a property you can put your own stamp on, you’re in the driver's seat. You aren't just buying an asset; you're crafting it for maximum cash flow and appeal. Before you go all-in, it’s a smart move to fully understand the property’s boundaries and potential quirks by learning what is involved in a property survey.

My clients get access to proprietary visualization tools that take the guesswork out of renovating. We can digitally test out different finishes, color schemes, and layouts before you spend a dime, making sure the final product aligns perfectly with your vision and financial goals.

Let's Find Your Next Investment

With my hands-on approach, we can zero in on properties in Baltimore County and Harford County that are ripe with potential. We'll find a house with great bones and then work together to design a beautiful, profitable rental that tenants will love.

If you’re ready to stop settling for what’s on the market and start creating a high-performing investment, let's talk.

Even after you've done your homework, a few questions are bound to pop up. It happens to everyone! Let's clear the air on some of the most common things I hear from new investors trying to figure out financing.

So, How Much Do I Really Need for a Down Payment?

Let's get straight to it: for a standard investment property loan, you're almost always looking at a down payment of 20-25%. Lenders simply see rentals as a bigger risk than the home you live in, so they want you to have more skin in the game.

But there are definitely ways to get creative. A popular strategy is "house hacking" a duplex or triplex. If you live in one unit and rent the others, you can often use an FHA loan and get in the door with as little as 3.5% down. It's a game-changer.

Can I Actually Use the Rent I Haven't Even Collected Yet to Qualify?

You bet, and this is a massive advantage for investors. Most lenders will let you count about 75% of the property's projected rental income toward your qualifying income. This can make all the difference in meeting their debt-to-income (DTI) requirements.

How do you prove it? You'll need one of two things: either a signed lease agreement if you already have a tenant lined up, or a professional rental appraisal (the bank will order what's called a Form 1007) that gives an official estimate of the fair market rent. This little trick is often what pushes an application over the finish line.

Is Getting a Loan for a Rental That Much Harder?

Honestly, yes, the bar is a little higher. Lenders are more cautious with investment properties.

They typically want to see:

A higher credit score.

A lower DTI ratio.

More cash reserves on hand—usually enough to cover six months of mortgage payments.

It’s definitely stricter than when you bought your own home, but being organized and prepared makes it a completely manageable process. And remember, once you’re up and running, understanding the available rental property tax deductions is key to boosting your actual take-home profit.

At Customize Your Home, I do more than just help you find a property. I give my clients visualization tools and hands-on service to design a rental that stands out and attracts top-tier tenants from day one. If you're looking in Baltimore or Harford County, let's talk about building a profitable investment. Visit https://www.customizeyourhome.com to get started.

Comments