What Is Homestead Tax Exemption Explained

- Justin McCurdy

- Dec 2, 2025

- 12 min read

Welcome to homeownership! It’s a huge step, and it comes with some amazing financial perks. One of the absolute best is the homestead tax exemption. This is a legal provision that can seriously reduce the taxable value of your main home, which means a lower property tax bill for you every year.

Think of it as a friendly discount on your taxes, designed to make owning your home a little easier on your wallet.

Your Guide to the Homestead Tax Exemption

So, what exactly is the homestead tax exemption? Let's break it down in a simple, friendly way.

Imagine your property's value is like a hot air balloon, always trying to float higher as the market changes. The homestead exemption is like a rope tethering that balloon, keeping its taxable value from rising too quickly. It's a legal safeguard that limits how much your property's assessment can increase each year, protecting you from getting hit with a massive, unexpected tax hike.

This isn't some secret loophole. It's a standard benefit for anyone who lives in their home as their primary residence. If you're a new homebuyer in fantastic communities like White Marsh, Edgewood, or anywhere in Baltimore County and Harford County, this is a must-have tool for keeping your housing costs stable. Getting a handle on this is just as important as choosing the right mortgage. Speaking of which, you can learn more about your financing options in our guide to home loan types explained for Maryland buyers.

How This Tax Break Works

The whole point is to shield a part of your home's value from being taxed. The exact rules change from state to state, but the outcome is always the same: you pay taxes on less than your home's full market value.

A homestead exemption directly lowers your property tax burden by excluding a portion of your home’s assessed value from taxation, ensuring your primary residence remains more affordable over the long term.

Here’s a practical, everyday example. Let's say your home is valued at $400,000, and you get an exemption that covers $50,000 of that value. You'll only be taxed on $350,000. If your local tax rate is 1%, that exemption just saved you $500 for the year. And that's every single year!

Those savings really add up, making property taxes a bit fairer for regular homeowners. You can discover more insights about how homestead exemptions work on SmartAsset.com. That's extra money you can put toward customizing your home with new flooring, countertops, cabinets, or whatever else is on your wish list.

How The Homestead Exemption Saves You Money

Alright, so we know what a homestead exemption is, but let's get down to the nitty-gritty: how does it actually save you money? It's all about putting a cap on how much your property's taxable value can shoot up each year.

This is a huge deal. It doesn't change what your home is actually worth on the open market, but it does limit the slice of that value the government can tax. Think of it as a financial shock absorber, keeping your property tax bills from giving you whiplash when the local real estate market gets hot.

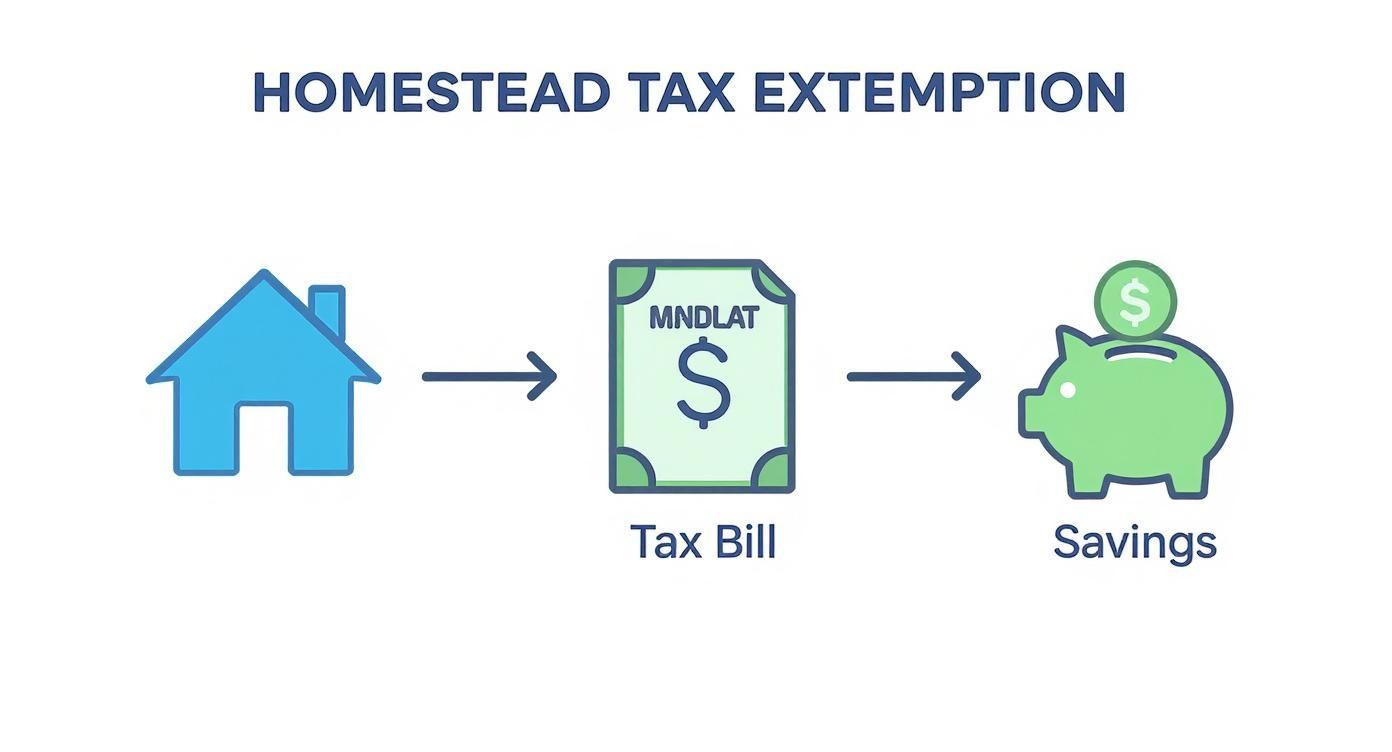

This simple diagram breaks down how the exemption translates into real savings in your bank account.

The path is pretty straightforward: you own a home, you apply for the exemption, and it directly trims your tax bill. More savings for you.

A Real-World Maryland Example

Let’s put some real numbers to this. Picture this: you’ve just settled into a beautiful new home in White Marsh, a great community in Baltimore County, Maryland.

Year 1: The county assesses your home's value at $400,000. With a sample property tax rate of 1.1%, your first annual tax bill comes out to $4,400.

Year 2: The market is booming! Your home’s assessed value jumps to $450,000. Without any protection, your tax bill would soar to $4,950—that's an extra $550 out of your pocket!

This is where Maryland's Homestead Tax Credit swoops in to save the day. The state puts a hard cap on how much your taxable assessment can increase in a single year—in this case, 10% for state taxes (and often even less for county taxes).

Instead of getting taxed on the full $450,000, the law says your taxable value can only go up by 10% from the previous year. That means your new taxable value is just $440,000 ($400,000 + 10%).

So, your new tax bill is based on $440,000, not the full $450,000. The bill becomes $4,840, instantly saving you $110 for the year. It might not seem like a life-changing amount at first, but this benefit stacks up year after year, shielding you from bigger and bigger tax hikes and helping you build financial stability.

Let's look at this comparison side-by-side to see the direct impact.

Homestead Exemption Savings At A Glance

Scenario | Assessed Home Value | Taxable Value | Property Tax Rate (Example) | Annual Tax Bill | Annual Savings |

|---|---|---|---|---|---|

Without Homestead Exemption | $450,000 | $450,000 | 1.1% | $4,950 | $0 |

With Homestead Exemption | $450,000 | $440,000 | 1.1% | $4,840 | $110 |

As the table shows, that $10,000 difference in taxable value translates directly into cash savings. Over time, as your home's value continues to climb, this protected gap widens, and your savings grow right along with it.

Mastering concepts like this is crucial for building real wealth through your property. To dig deeper, you should check out our guide on what is home equity and how does it actually work.

And remember, property tax isn't the only place to find savings. If you're self-employed, for instance, you can look into other powerful ways to lower your taxable income, like the self-employed health insurance deduction. Every dollar you save is another dollar you can put toward making your home truly yours.

Qualifying for the Homestead Exemption in Maryland

So, you're sold on the idea of saving some serious cash—who isn't? The next logical question is, do you actually qualify for this fantastic tax break? The good news is that for most new homeowners in Maryland, from Edgewood to White Marsh, the process is refreshingly simple.

The whole point of the homestead exemption is to help everyday homeowners, not professional real estate investors. Let's walk through exactly what you'll need to have in place.

The Core Requirements

Think of this as your basic eligibility checklist. To get the green light for Maryland's Homestead Tax Credit, you really only need to nail down two main things.

You Must Own the Property: This one’s a no-brainer. Your name has to be on the deed. This simply proves you're the legal owner of the home, not just renting it.

It Must Be Your Principal Residence: This is the big one. The homestead exemption is strictly for the home you actually live in full-time. It’s your main "home base"—the address on your driver's license, where your mail gets delivered, and where you're registered to vote.

Basically, this tax break isn’t for your beach house, mountain cabin, or any rental properties you might own. It’s all about making the home you live in more affordable.

Special Considerations and Extra Benefits

On top of the standard requirements, some situations can open the door to even more tax relief. While the main homestead credit is for pretty much all qualifying homeowners, Maryland has some extra programs to support specific groups.

Across the country, homestead exemptions help millions of homeowners every single year. The savings can be huge, but they vary a ton from state to state. More than 40 states offer some version of this benefit, often with bigger breaks for seniors, veterans, or disabled homeowners. For new buyers, getting a handle on these rules is just smart homeownership. You can read more about how homestead exemptions vary by state on the Alabama Department of Revenue's site.

For instance, Maryland offers property tax exemptions for 100% disabled veterans and their surviving spouses. There are also a handful of programs designed to help seniors stay in their homes without being overwhelmed by property taxes. The rules for these are a bit more detailed, so your best bet is to always check the official Maryland Department of Assessments and Taxation (SDAT) website for the latest info.

Figuring out if you qualify is the first big step toward locking in these savings. If you're just getting started, our guide on how to buy your first home in Maryland is a great resource for the entire journey. Once you've confirmed you meet the criteria, it's time to tackle the simple application, which we'll cover next.

A Simple Guide to Applying in Maryland

So, you know you qualify. Great! Now, let’s get those savings locked in. The good news is that applying for the Maryland Homestead Tax Credit is surprisingly easy, and you can get it done right after you’ve closed on your new home in a community like White Marsh or Edgewood.

This is a one-time application that keeps paying off year after year by helping keep your property tax bill from getting out of control. The whole thing is handled by the Maryland Department of Assessments and Taxation (SDAT), and they’ve made the process pretty painless, whether you do it online or by mail. Just think of it as the last bit of paperwork before you can officially start saving money.

Your Step-by-Step Application Checklist

Ready to check this off your list? Here’s a simple rundown of exactly what you need to do to claim your homestead tax credit.

Find Your Property Account Number: First things first, you'll need this unique number. It should be on the settlement paperwork you got at closing. If you can't find it, no worries—just look up your address on the official SDAT Real Property Data Search website.

Get the Application: You’ve got a couple of options here. The fastest way is to fill it out directly on their online portal. If you prefer paper, you can download and print the application form right from the SDAT site.

Fill Out the Form: The form itself is short and sweet. It just asks for basic info like your property address, that account number you just found, and for you to confirm that this house is, in fact, your primary home.

Submit It: If you filed online, you’ll get a confirmation right away. If you mailed it in, just send the completed form to the SDAT Homestead Eligibility Section—the address is listed right on the form.

The whole process is designed to be quick, so you can move on to the fun stuff, like using our visualization tools to decide on the perfect finishes for your new kitchen.

Key Deadlines You Cannot Miss

With taxes, timing is everything. To make sure your homestead credit applies to the next tax year, you absolutely have to get your application in on time.

The hard deadline to file your Maryland Homestead Tax Credit Application is December 31st. If you get it in by then, your credit will be applied to the next taxable year, which starts on July 1st.

If you miss that date, you'll have to wait an entire extra year to see those savings kick in. My advice? Apply as soon as you get settled. For instance, if you buy a home in Baltimore County in August 2024 and apply before December 31, 2024, your tax credit will be applied starting July 1, 2025.

Once you're approved, you're done. The credit renews automatically every year as long as the house is still your main residence. You don't have to reapply, which makes it a fantastic set-it-and-forget-it benefit.

Homestead Laws Protect More Than Your Wallet

The homestead tax exemption is a fantastic perk for lowering your property tax bill, but its benefits run much deeper than just annual savings. The whole idea of a "homestead" is built on a powerful foundation: protecting you and your family.

This legal tradition sees your primary home as more than just an asset; it's your sanctuary. Historically, these laws were created to stop creditors from seizing a family's home during tough financial times. So, beyond the tax credit, your home has a legal shield against most debts, making sure you have a roof over your head even when life throws you a curveball.

A Shield for Your Biggest Asset

Think of it like a legal fortress around your home. Rooted deep in U.S. law, these protections prevent your home from being forcibly sold to pay off most debts. The main exceptions are your mortgage, property taxes, or liens from contractors who worked on your house.

This means a financial misstep won’t automatically cost you your family's home. It’s a powerful tool that safeguards your equity and stability. You can learn more about the history of homestead protections at Rocket Mortgage.

The whole point behind homestead laws is to keep the family home as a place of refuge. It reinforces that your home is a source of stability, backed by a long-standing legal tradition designed to protect families through thick and thin.

State-Specific Protections

Now, how strong that protective shield is really depends on where you live. Each state has its own take.

For example, some states offer nearly unlimited protection for your home's value, while others cap it at a specific dollar amount. The legal protections can also be tied to other local rules, like whether you live in a state with specific community property state rules, which can change how exemptions are handled, especially for married couples.

Understanding this protective side of homeownership is empowering. It’s a great reminder that when you buy a home in a place like Harford County or Baltimore County, you aren't just making a financial investment. You're building a stable future for your family, with laws in place to help you protect it.

Turn Tax Savings Into Your Dream Home

Smart financial moves are what turn a house into a happy, comfortable home. Applying for the homestead exemption is one of those easy wins that just keeps paying you back, year after year. The real question is, what will you do with that extra cash?

Think about it. That money could be the exact amount you need to say "yes" to those gorgeous hardwood floors you saw, or maybe it's the boost that lets you upgrade from laminate to the quartz countertops you've been dreaming of. My goal isn't just to help you buy a house; it's to help you create a home that truly feels like you, without breaking the bank.

From Savings to Style

With my hands-on service and unique proprietary visualization tools, we can play around with different finishes and see exactly how they'll look in your new home, whether it's in White Marsh or Edgewood. It’s all about making savvy choices that improve your daily life and add value to your investment.

We can use clever savings strategies, like the homestead credit, to make room in the budget for the custom touches that really matter to you—like picking your favorite flooring, countertops, and cabinets. This is what smart financial planning for homeownership looks like.

When you pair tax credits with solid saving habits, you're setting yourself up for success. For more on that, take a look at our guide on how to save for a down payment.

Ready to get started? Let’s connect and start turning your ideas into a reality.

Got Questions About the Homestead Exemption?

Jumping into the world of property taxes can feel a little overwhelming, especially when you're a new homeowner. Let's clear up some of the most common questions folks have about the homestead tax exemption here in Maryland.

Do I Have to Reapply Every Year?

Nope, you can breathe a sigh of relief on this one. Once your application for the Maryland Homestead Tax Credit is approved, it automatically renews every year.

You can set it and forget it, knowing that benefit is locked in as long as you continue to own and live in the property as your main home. The only time you'd need to do anything is if your living situation or ownership status changes.

What’s the Application Deadline?

My best advice? Apply as soon as you close on your new home! The official deadline to get your application in is December 31st.

Hitting that date ensures your credit kicks in for the next taxable year, which starts on July 1st. If you happen to miss it, you'll have to wait a whole extra year for the savings to start, so it really pays not to put this on the back burner.

Can I Use This Exemption on a Rental Property?

That's a definite no. The homestead exemption is strictly for your principal residence—the home you actually live in full-time.

It can't be used for vacation homes, second homes, or any rental or investment properties you might own. The whole point of the program is to give a little relief to primary homeowners and make things more affordable.

How Does This Help if My Home's Value Skyrockets?

This is where the homestead credit really becomes your best friend, especially in a hot real estate market. Its main job is to shield you from huge, unexpected spikes in your property tax bill.

The Maryland Homestead Tax Credit puts a ceiling on how much your taxable assessment can go up each year. It’s capped at a maximum of 10% for state property taxes, and often even less for county taxes.

So, let's say your home's market value in a community like White Marsh or Edgewood jumps by 20% in a single year. Your tax bill won't reflect that massive leap. That cap acts as a critical buffer, keeping your payments predictable and protecting your household budget from sticker shock.

While the builder I represent provides high-quality homes, I go a step further—offering my clients unique proprietary visualization tools, hands-on service, and access to visualizers that help you bring your dream space to life. We let buyers customize their homes by getting to pick their flooring, countertops, cabinets, tile, and more. Let's create a home that is truly you. Visit https://www.customizeyourhome.com to get started.

Comments